Jayanagar 3rd Block East Bangalore-560011, Karnataka India

Insurance Case Study: Murder or Accident? Court Ruled

Insurance Case Study: Murder, Not Accident? Insurer Denied Claim — Court Disagreed

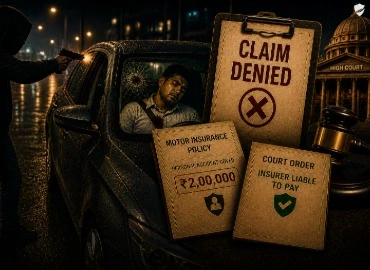

Insurance claim disputes often become complicated when insurers and nominees disagree on the actual cause of death. One of the most debated issues in accidental death insurance is whether a murder can legally be treated as an accident under a personal accident insurance policy. In this insurance case study, an insurer reportedly rejected an accidental death claim by arguing that the insured's death was a case of murder and therefore not covered under the policy. However, the court reportedly disagreed with the insurer's interpretation and ruled in favor of the nominee. The case became an important example of how courts interpret accidental death insurance claims in complex legal situations involving homicide and insurance liability.

Insurer Rejected the Claim Saying It Was Murder, Not an Accident

According to reports surrounding the dispute, the nominee filed a personal accident insurance claim after the insured person died under violent circumstances.

The insurer reportedly denied the accidental death benefit claim by arguing that:

In many accidental death insurance disputes, insurers examine:

This led to a major insurance dispute after the nominee challenged the rejection decision.

Personal Accident Insurance Claim Turned Into a Legal Battle

After the insurer allegedly denied the claim, the nominee reportedly approached the appropriate legal forum seeking compensation under the personal accident insurance policy.

The dispute reportedly centered around a key legal issue: Can a murder ever be treated as an accidental death for insurance purposes?

The nominee reportedly argued that:

Several Indian court rulings and consumer commission decisions have observed that murder may still qualify as accidental death if the insured was not the aggressor or deliberate participant in the incident.

The case soon evolved into a significant legal battle involving accidental death insurance liability.

Court Reviewed Policy Terms, Liability, and Cause of Death

During the proceedings, the court reportedly examined:

Courts in accidental death insurance disputes often apply the principle that if the insured did not deliberately invite or participate in the fatal act, the resulting death may still qualify as accidental.

The court reportedly reviewed whether the insured was specifically targeted intentionally, whether the death occurred unexpectedly, and whether the policy expressly excluded murder-related claims.

The matter highlighted how legal interpretation of insurance contracts can significantly affect compensation outcomes in accidental death cases.

Judgment Favored the Nominee in the Insurance Dispute

According to the reported outcome, the court reportedly ruled in favor of the nominee and disagreed with the insurer's rejection of the accidental death claim.

The ruling reportedly emphasized that:

The judgment became an important reference point in discussions involving accidental death insurance claims, personal accident insurance disputes, murder vs accident insurance interpretation, and insurance claim rejection challenges.

Lessons From This Accidental Death Insurance Case Study

This insurance case study offers several important lessons for policyholders and nominees.

| # | Key Lesson | What It Means |

|---|---|---|

| 1 | Policy Wording Matters | Insurance coverage depends heavily on the exact wording of policy definitions and exclusions. |

| 2 | Not Every Murder Is Automatically Excluded | Courts may interpret certain homicide cases as accidental death depending on the circumstances. |

| 3 | Documentation Is Extremely Important | FIRs, postmortem reports, medical records, and investigation documents play a major role in claim disputes. |

| 4 | Claim Rejections Can Be Challenged | Nominees may approach consumer forums or courts if they believe the insurer unfairly rejected the claim. |

| 5 | Legal Interpretation Can Change Claim Outcomes | Insurance disputes often depend on judicial interpretation of policy terms and factual circumstances. |

Conclusion

This insurance case study involving a dispute over murder versus accidental death highlights how complex accidental death insurance claims can become when insurers and nominees interpret policy coverage differently.

Insurance claim disputes often arise from differing interpretations of policy terms and cause of death. Policyholders and families should understand accidental death coverage carefully and maintain proper legal and claim documentation.

At BasketOption.insure, we help policyholders and nominees understand their insurance rights and navigate complex claim disputes. Whether you need personal accident insurance guidance or help challenging a rejected claim, our experts are here. Visit https://basketoption.insure/ or get in touch with our experts today to explore insurance plans that truly care about your needs.

Latest Posts

Our Experts

Frequently Asked Questions

Understand accidental death insurance. Know your nominee rights. Stay protected.

?What is an accidental death insurance claim?

An accidental death insurance claim is a request for compensation under a policy that covers death caused by sudden, external, and unforeseen events.

?Can murder be treated as accidental death in insurance claims?

In certain cases, courts have held that murder may qualify as accidental death if the insured was not a deliberate participant or aggressor in the incident.

?Why do insurers reject accidental death claims in murder cases?

Insurers may argue that murder does not fall within the definition of an accident under the policy terms or that exclusions apply.

?What is a personal accident insurance policy?

A personal accident insurance policy provides financial compensation in cases involving accidental death, permanent disability, or serious injuries caused by accidents.

?What documents are important in accidental death insurance claims?

Important documents include FIRs, postmortem reports, death certificates, insurance policy documents, medical records, and nominee details.

?Can nominees legally challenge rejected insurance claims?

Yes, nominees may approach consumer forums, insurance ombudsmen, or courts if they believe the claim rejection was unfair.

?What factors do courts examine in accidental death disputes?

Courts generally examine cause of death, policy wording, circumstances surrounding the incident, and whether the insured deliberately contributed to the event.

?What lessons does this insurance case study teach policyholders?

This case highlights the importance of understanding accidental death coverage, reading exclusions carefully, maintaining documentation, and seeking legal advice in disputed claims.

?Why is the distinction between murder and accidental death important in insurance?

The classification can determine whether compensation is payable under accidental death or personal accident insurance policies.

?Why are accidental death insurance case studies important?

These case studies help policyholders understand real-world claim disputes, legal interpretations of insurance terms, and how courts examine complex accidental death claims.