Jayanagar 3rd Block East Bangalore-560011, Karnataka India

Insurance Case Study: ₹1,000 Draft Became ₹7 Lakhs

Insurance Case Study: ₹1,000 Demand Draft Was Turned Into ₹7 Lakh — Insurance Claim Dispute Reached Court

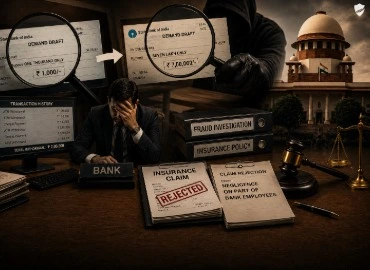

Financial fraud cases often begin with small irregularities that later uncover massive losses and complex legal disputes. In this insurance case study, a demand draft reportedly issued for just ₹1,000 allegedly became a multi-lakh banking dispute after its amount was altered to nearly ₹7 lakh. The incident triggered questions about fraud detection, banking negligence, forged financial instruments, and insurance liability. The dispute eventually escalated into court proceedings, highlighting the growing risks of cheque and demand draft fraud in the banking system.

A ₹1,000 Demand Draft Turned Into a Multi-Lakh Dispute

The case reportedly began with a demand draft originally issued for ₹1,000. However, during processing and banking transactions, the amount on the instrument was allegedly altered to approximately ₹7 lakh.

Such cases involving altered financial instruments can lead to significant financial losses for banks, businesses, and customers. Fraud involving demand drafts, cheques, and negotiable instruments often raises concerns about:

This altered demand draft case study later became a major example of how even small banking instruments can result in serious financial fraud disputes.

How the Alleged Financial Fraud Was Discovered

The alleged fraud reportedly came to light during banking verification and transaction review processes. Authorities and financial institutions began examining whether the demand draft had been tampered with before clearance.

In financial fraud insurance disputes, investigations generally focus on:

Demand draft fraud cases often involve allegations related to:

The incident also highlighted the growing importance of fraud prevention systems in modern banking operations.

Insurance Claim and Banking Liability Came Under Scrutiny

Following the discovery of the alleged fraud, an insurance claim dispute reportedly emerged regarding who would bear responsibility for the financial loss.

The dispute involved questions such as:

Financial crime insurance policies may provide protection against losses caused by forgery, employee dishonesty, fraudulent financial instruments, and theft and financial manipulation. However, disputes often arise regarding policy exclusions, negligence, procedural failures, and fraud detection responsibilities.

Court Examined Forgery, Compensation, and Responsibility

As the dispute intensified, the matter reportedly reached court for legal examination. The court reviewed various aspects related to the alleged financial fraud and the resulting insurance claim dispute.

The proceedings reportedly involved examination of:

Courts in banking fraud insurance disputes often examine whether reasonable verification measures were followed, whether internal controls were adequate, whether the fraud could have been prevented, and whether the insurance policy covered the financial loss.

The case highlighted how forged financial instrument disputes can quickly evolve into large-scale legal and insurance battles involving substantial financial exposure.

What This Insurance Case Study Reveals About Banking Fraud Risks

This financial fraud insurance case study offers several important lessons for banks, businesses, insurers, and financial institutions.

| # | Key Lesson | What It Means |

|---|---|---|

| 1 | Even Small Financial Instruments Can Lead to Major Losses | A seemingly minor banking instrument can become the center of a significant fraud and compensation dispute if safeguards fail. |

| 2 | Fraud Detection Systems Are Critical | Banks and institutions must implement strong verification procedures and fraud monitoring systems. |

| 3 | Insurance Coverage Must Be Carefully Reviewed | Financial crime insurance policies should clearly address forgery, fraud, and internal liability risks. |

| 4 | Documentation and Verification Matter | Accurate recordkeeping and verification processes play a major role in preventing financial fraud disputes. |

| 5 | Negligence Can Increase Legal Liability | Failure to follow proper banking procedures may expose institutions to legal claims and compensation disputes. |

Conclusion

This insurance case study involving a ₹1,000 demand draft allegedly altered into ₹7 lakh demonstrates how banking fraud can trigger complex insurance disputes and legal proceedings.

Financial fraud can happen through even small banking instruments if security checks fail. Businesses and financial institutions must strengthen fraud detection systems, document verification processes, and insurance protection against financial crimes.

At BasketOption.insure, we help businesses get the right financial crime and liability insurance coverage. Whether you're a financial institution, business owner, or individual seeking protection, our experts are ready to help. Visit https://basketoption.insure/ or get in touch with our experts today to explore insurance plans that truly care about your needs.

Latest Posts

Our Experts

Frequently Asked Questions

Understand financial fraud risks. Protect your business. Stay insured.

?What is a demand draft fraud case?

A demand draft fraud case involves alteration, forgery, or unauthorized manipulation of a demand draft to illegally obtain money or cause financial loss.

?How can a demand draft be altered fraudulently?

Fraudsters may attempt to change the amount, beneficiary details, or other information on financial instruments through forgery or tampering.

?What is a bank fraud insurance claim?

A bank fraud insurance claim is a claim filed to recover financial losses arising from fraud, forgery, employee dishonesty, or other financial crimes.

?Can insurance disputes arise after banking fraud?

Yes, disputes may arise regarding coverage terms, negligence, fraud detection responsibilities, and liability for financial losses.

?Why are forged financial instrument cases legally significant?

Such cases involve questions related to negligence, verification failures, fraud prevention, financial liability, and insurance coverage.

?What documents are important in financial fraud insurance disputes?

Important documents include demand draft copies, banking transaction records, forensic or handwriting reports, insurance policy documents, internal verification records, and investigation reports.

?Can banks be held liable in altered demand draft cases?

Banks may face liability if negligence in verification, processing, or fraud detection contributed to the financial loss.

?What lessons does this insurance case study teach financial institutions?

This case highlights the importance of strong fraud detection systems, proper verification procedures, employee training and compliance, timely reporting of suspicious transactions, and adequate financial crime insurance coverage.

?What is financial crime insurance?

Financial crime insurance helps protect businesses and institutions against losses caused by fraud, forgery, theft, cybercrime, or employee dishonesty.

?Why are insurance case studies important in banking and finance?

Insurance case studies help banks, businesses, and professionals understand real-world fraud risks, legal disputes, liability issues, and the importance of insurance protection against financial losses.